Success Story from Glenn B. and a Question

By Dave Mabe

Here's an update from MabeKit user Glenn B., and a question (name used with permission, lightly edited for clarity)

Glenn B.

I've recently completed my first model, thanks to MabeKit.

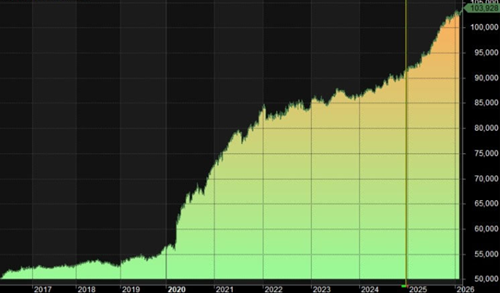

Below are my first successful strategy, which probably has some mistakes, but the insights from this process are immeasurable!

Crunched 3 times:

To be honest, I'm MORE happy about the process I've developed to build a new strategy than I am about this particular one.

With reduced self-inflicted coding bottlenecks, I'm really focusing on the data and the bigger picture.

My time is spent more on questions like:

What does the data say about timed exits?

What does the data say about risk management?

What can't my data tell me?

How can I validate the results?

etc...

All my preconceived notions have been abandoned, and I'm feeling pretty hyped about my new perspective!

My main question: in your experience, what percentage of completed models will pass paper/live trading?

Dave:

Nice work, Glenn! You're right: the power here isn't necessarily in any one particular strategy, but in a generic process for building reliable strategies.

And your mindset at this particular point in the process is ideal!

Most traders at this point feel like the work is done - the equity curve looks good, and it's off to the races.

But a healthy dose of skepticism at this point will take you a long way.

The next phase is where the real learning begins.

The moment you go live, even at a minuscule size, you are getting feedback about your strategy from the best traders in the world in real-time.

How can I validate the results?

This is the right question to ask yourself.

The quicker you can validate your results, the quicker your path to confidence with the strategy.

This is one reason why backtesting is so powerful.

Think about discretionary trading - it might take you months or years to get confident enough in a strategy to trade it responsibly with large size.

That's because there is no way to validate the results of a discretionary strategy quickly.

But back to your question. First, there are no "completed" models - there's always some way to improve them.

And there is no pass/fail test for live trading, there's just varying confidence in the strategy over time.

The real question to ask yourself: what questions would I need to answer to trade this strategy with bigger size?

More on this topic in the coming days...

Congrats, Glenn, and thanks for sharing with the list!

-Dave

P.S. Do you wish you had a strategy that actually made money? Create your own in minutes, not months with MabeKit