Recency Matters

By Dave Mabe

In general, the more recent the action, the more predictive it can be in your strategy.

Here's a good example from a strategy I'm working on.

It's a short strategy based on gapping stocks.

I've run a broad backtest in Amibroker with the MabeKit column library applied, and I've run it through the Strategy Cruncher.

This is the first optimization I've run on the strategy.

Among the suggestions in the Cruncher report, here are two that stick out to me.

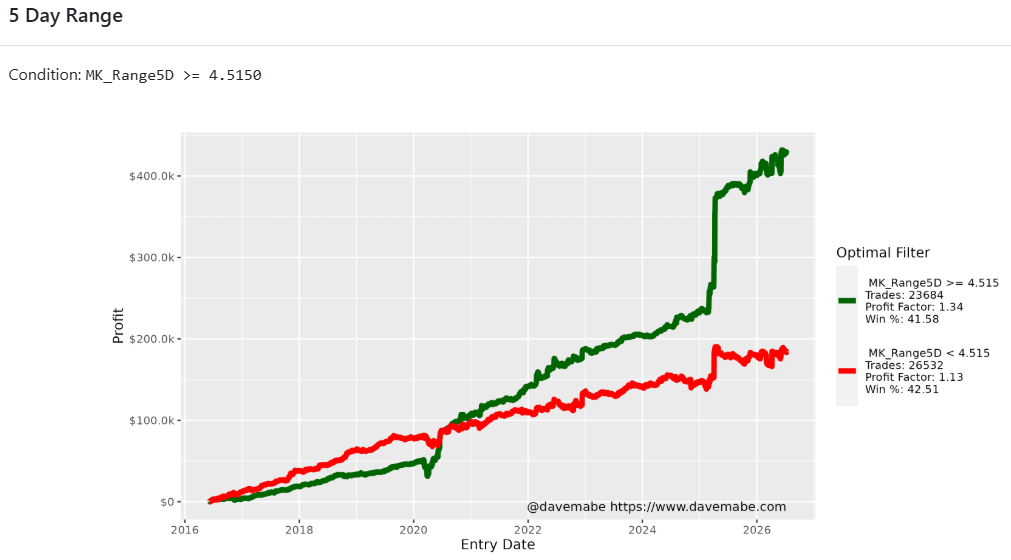

The 5 day range:

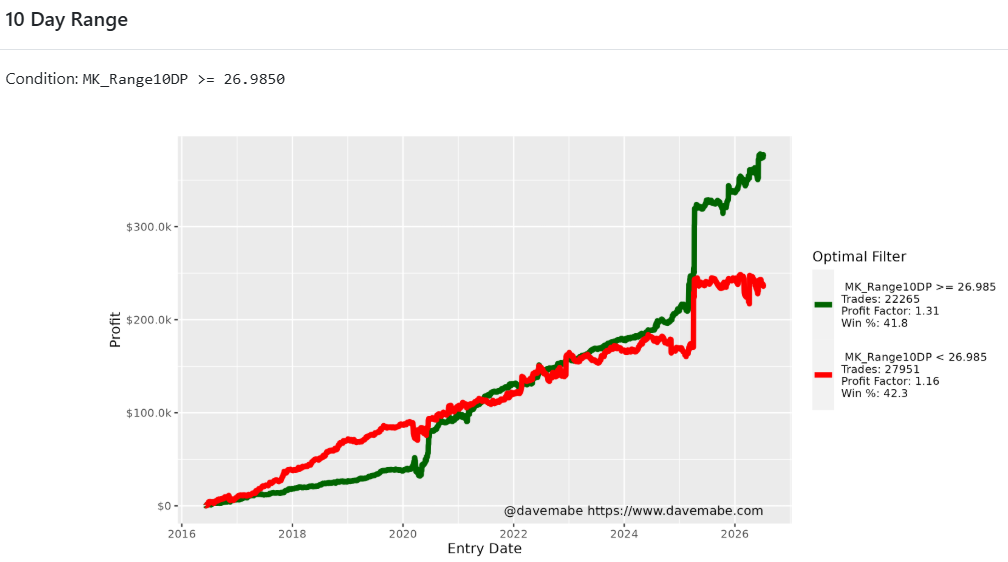

And the 10 day range:

There are a couple of things to point out here.

Assuming you want to apply one of these rules to your strategy, how do you decide?

There is a slight difference in the curves here, but not enough to be significant.

Also note that these filters are highly correlated - one is describing the 5 day range and the other the 10 day range.

When using the Strategy Cruncher to create a strategy, you are often confronted with this situation.

Both of these suggestions are telling you the same thing - the higher the recent daily range, the better the trades perform.

Just like in baseball, where the tie goes to the runner, I almost always defer to the filter that reflects more recent trading activity - in this case, the 5 day range.

Think of two extremes: the daily range yesterday versus the range of the last 200 days.

Which is more likely to contribute something predictive to trading action in your strategy NOW?

Which can contribute more to your path to confidence with this strategy?

-Dave

P.S. Do you wish you had a column library that would tell YOU how to make your strategy profitable? My column library is now included with MabeKit Get Instant Access