A Backtest With and Without Delisted Stocks

By Dave Mabe

Since I've created a tool to update my backtesting database in the most efficient way possible (download it for free here), I now have two backtesting databases.

One contains data from IQFeed, where I've not attempted to include delisted symbols.

Another one has data from Massive/Polygon, which includes delisted symbols and resolves splits automatically.

Now that I have this data available at my fingertips, I can run the same backtest across either Amibroker database.

So what did I find?

Were there fundamental differences that I was completely unaware of by not including delisted symbols?

Did my strategy fall apart when I finally did it "the right way"?

Not exactly.

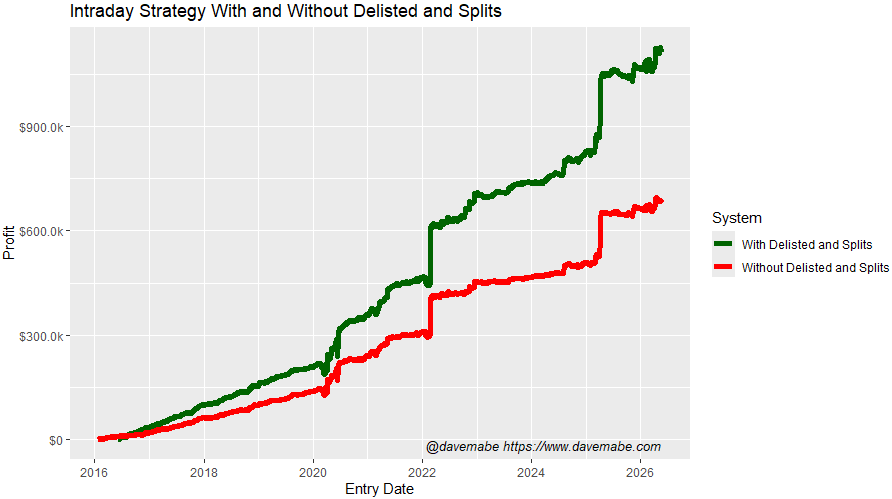

Here's one of my intraday strategy starting points, before optimization:

The green line looks better, right?

Well, that's not telling the whole story - because it includes delisted stocks, there are obviously going to be more trades.

But are the results fundamentally different?

Here are some stats comparing the two:

Without Delisted and Splits:

Number of Trades: 55,910

Profit Factor: 1.23 (the Strategy Cruncher improves this to over 2.0 for my go-live version)

Win Rate: 41.7% (the Strategy Cruncher improves this to ~50% for my go-live version)

With Delisted and Splits:

Number of Trades: 83,171

Profit Factor: 1.25

Win Rate: 41.0%

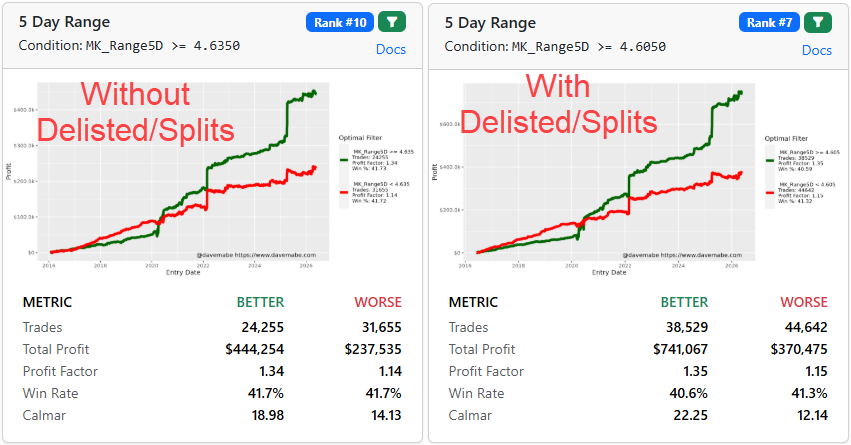

When I run these separately through the MabeKit Strategy Cruncher, there are some minor differences, but the optimization path is essentially unchanged.

For example, here's a column included with the MabeKit column library across both reports.

Basically the same.

This confirms my theory that I wasn't missing anything by not including delisted stocks.

Of course, it's a completely different story if you're holding positions overnight!

One more reason I prefer day trading to swing trading.

-Dave

P.S. Are you in a drawdown and ready to quit? Join the other traders who reversed their drawdowns and are printing money with MabeKit.